41 yield of zero coupon bond

How to Buy Zero Coupon Bonds | Finance - Zacks The less you pay for a zero coupon bond, the higher the yield. A bond with a face value of $1,000 purchased for $600 will yield $400 at maturity. Zero coupon bonds are issued by the Treasury ... How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816)

What Is a Zero Coupon Yield Curve? - Smart Capital Mind The zero coupon rate is the return, or yield, on a bond corresponding to a single cash payment at a particular time in the future. This would represent the return on an investment in a zero coupon bond with a particular time to maturity. The zero coupon yield curve shows in graphical form the rates of return on zero coupon bonds with different ...

/dotdash_Final_Par_Yield_Curve_Apr_2020-01-3d27bef7ca0c4320ae2a5699fb798f47.jpg)

Yield of zero coupon bond

Zero Coupon Bond: Meaning, Features & Advantages - BondsIndia A zero-coupon bond is a debt instrument wherein the issuer does not make any coupon payment but instead trades at a deep discount, rendering a profit at maturity, when the bond is redeemed for its full-face value. A zero-coupon bond will usually have higher returns than a regular bond with the same maturity because of the shape of the yield curve. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

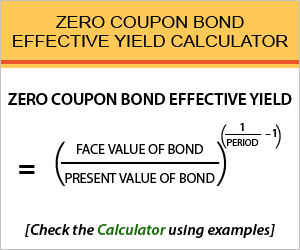

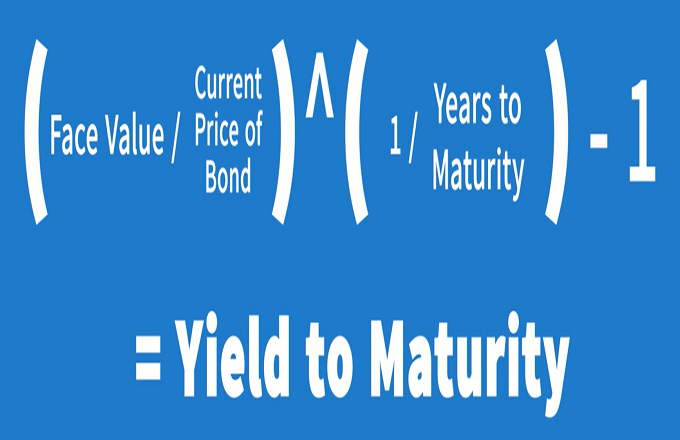

Yield of zero coupon bond. Solved A 12.75-year-maturity zero-coupon bond selling at a | Chegg.com A 12.75-year-maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 150.3 and modified duration of 11.81 years. A 30 -year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-11.79 years-but considerably higher convexity of 231.2. Bootstrapping | How to Construct a Zero Coupon Yield Curve in Excel? The annual coupon payment is depicted by multiplying the bond's face value with the coupon rate. read more. Hence, the spot rate for the 6-month zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a discount to its par ... Zero Coupon Bond Calculator 【Yield & Formula】 - Nerd Counter Zero-Coupon Bond Yield = F 1/n PV - 1 Here; F represents the Face or Par Value PV represents the Present Value n represents the number of periods I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond. Zero Coupon Bond Yield - Formula (with Calculator) - finance formulas The formula for calculating the effective yield on a discount bond, or zero coupon bond, can be found by rearranging the present value of a zero coupon bond formula: This formula can be written as This formula will then become By subtracting 1 from the both sides, the result would be the formula shown at the top of the page. Return to Top

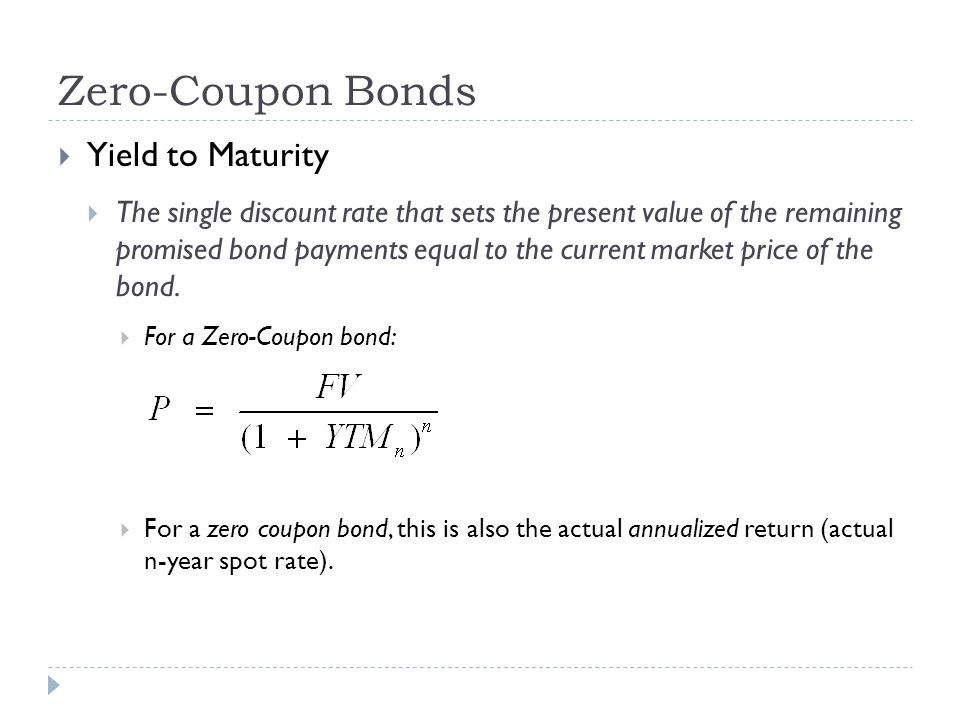

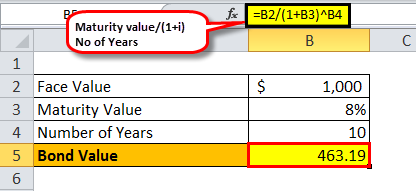

Value and Yield of a Zero-Coupon Bond | Formula & Example - XPLAIND.com The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value of Total Holding = 100 × $553.17 = $55,317 Expected accrued income = Value at the end of a period − Value at the start of a period Yield to maturity calculator - syuzyu.zurriyetsiz.info Yield to Maturity Calculator is an online tool for investment calculation , programmed to calculate the expected investment return of a bond. This calculator generates the output value of YTM in percentage according to the input values of YTM to select the bonds to invest in, Bond face value, Bond price, Coupon rate and years to maturity ... Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Calculating Yield to Maturity on a Zero-coupon Bond YTM = (M/P) 1/n - 1 variable definitions: YTM = yield to maturity, as a decimal (multiply it by 100 to convert it to percent) M = maturity value P = price n = years until maturity Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Zero Coupon Bond - (Definition, Formula, Examples, Calculations) The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years. Fitted Yield on a 10 Year Zero Coupon Bond (THREEFY10) Graph and download economic data for Fitted Yield on a 10 Year Zero Coupon Bond (THREEFY10) from 1990-01-02 to 2022-09-30 about 10-year, bonds, yield, interest rate, interest, rate, and USA. Yield Curves for Zero-Coupon Bonds - Bank of Canada These files contain daily yields curves for zero-coupon bonds, generated using pricing data for Government of Canada bonds and treasury bills. Each row is a single zero-coupon yield curve, with terms to maturity ranging from 0.25 years (column 1) to 30.00 years (column 120). The data are expressed as decimals (e.g. 0.0500 = 5.00% yield). A ... Primer: Par And Zero Coupon Yield Curves - Bond Economics Within a single currency, there are often several yield curves of interest. The relationship between the zero rate and the discount factor is: DF (t) = 1/ (1+r)^t, where DF is the discount factor, and r is the zero rate for maturity t (in years). One of the important properties of the discount factor is that it is equal to 1 at t=0.

Par Yield Curve Definition

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

1: Yield curves for Danish zero-coupon bonds. The red curve ...

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

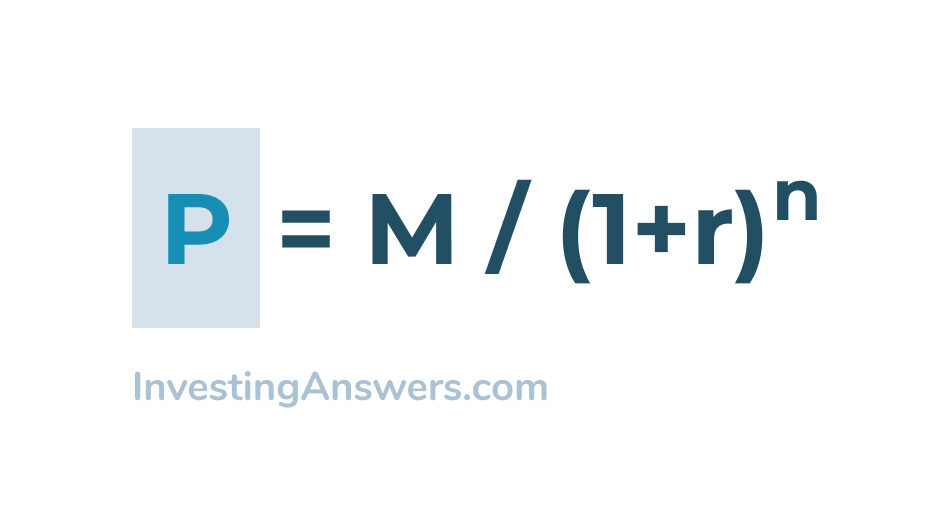

Zero Coupon Bond Definition and Example | Investing Answers

Zero Coupon Bond: Meaning, Features & Advantages - BondsIndia A zero-coupon bond is a debt instrument wherein the issuer does not make any coupon payment but instead trades at a deep discount, rendering a profit at maturity, when the bond is redeemed for its full-face value. A zero-coupon bond will usually have higher returns than a regular bond with the same maturity because of the shape of the yield curve.

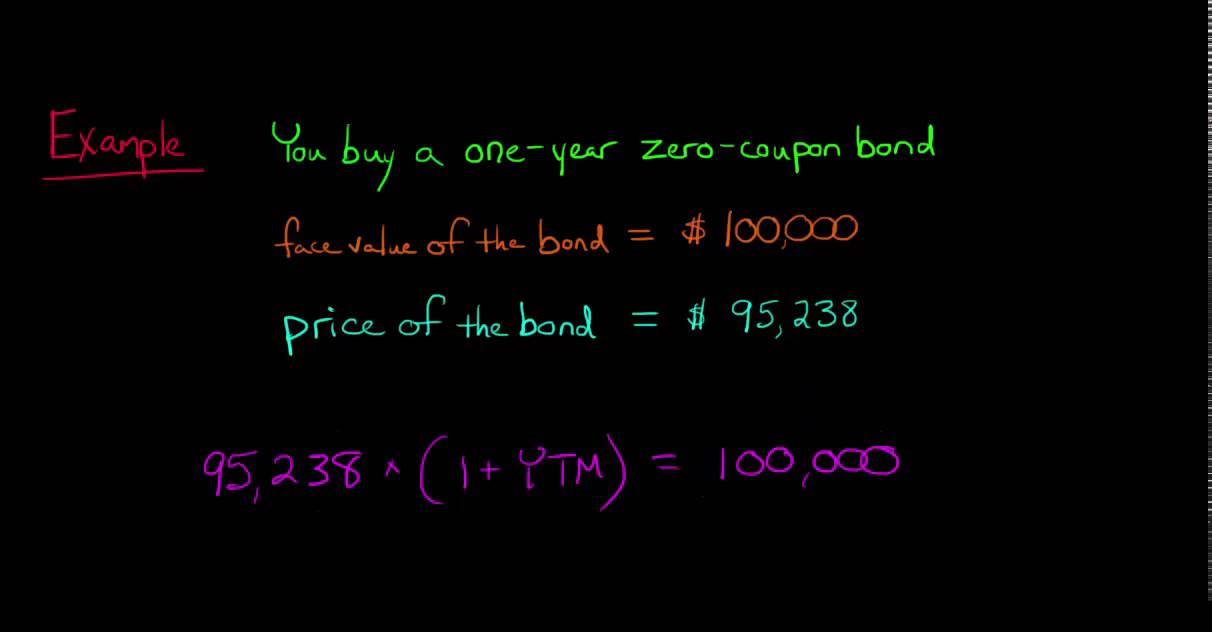

Calculating the Yield of a Zero Coupon Bond

Zero-Coupon Bond - an overview | ScienceDirect Topics

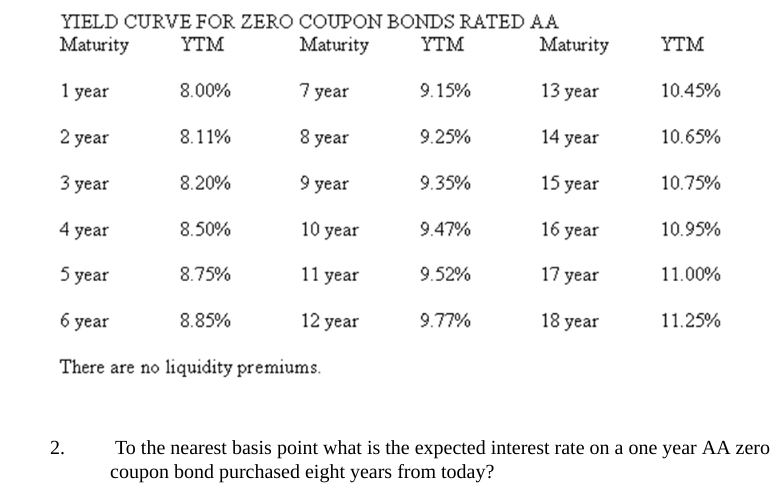

Solved YIELD CURVE FOR ZERO COUPON BONDS RATED AA Maturity ...

Zero Coupon Bonds

Fitted Yield on a 10 Year Zero Coupon Bond (THREEFY10) | FRED ...

ð‚ðšð¥ðœð®ð¥ðšðð¢ð§ð ðð¡ðž ð„ðŸðŸðžðœðð¢ð¯ðž ð˜ð¢ðžð¥ð ...

Primer: Par And Zero Coupon Yield Curves | Seeking Alpha

Zero-Coupon Bond - an overview | ScienceDirect Topics

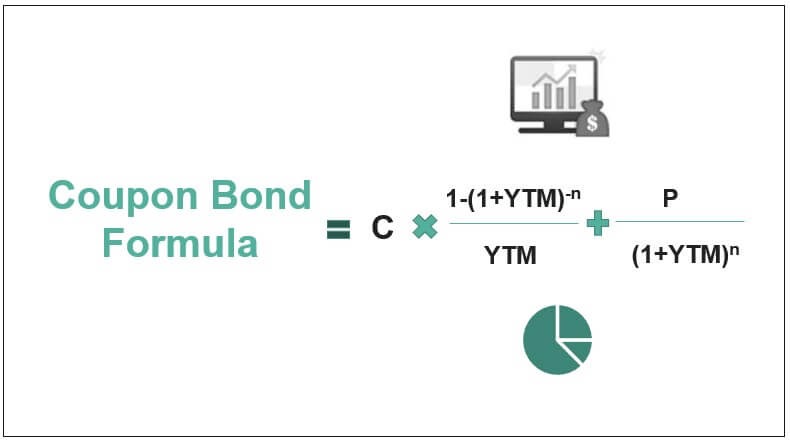

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

Zero Coupon Bond Yield Calculator - Find Formula, Example & more

Calculate the YTM of a Zero Coupon Bond

Zero Coupon Bond | Definition, Formula & Examples Video

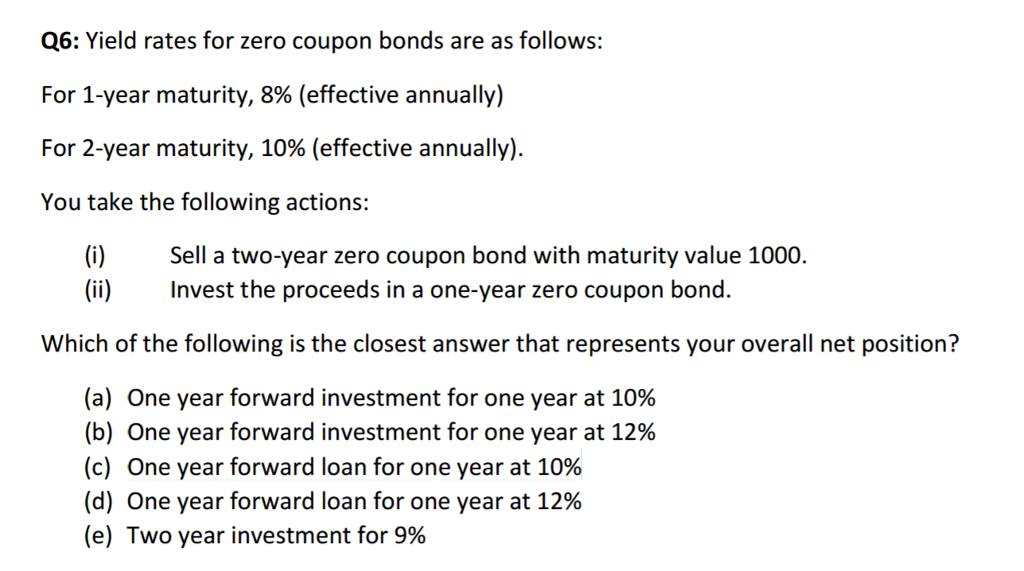

Solved Yield rates for zero coupon bonds are as follows: for ...

Zero-coupon yield curves estimated with the Nelson/Siegel ...

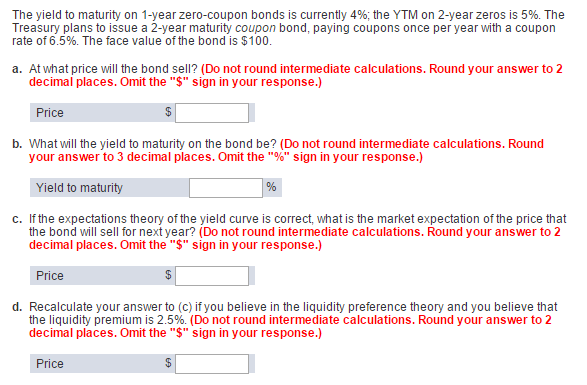

Solved The yield to maturity on 1-year zero-coupon bonds is ...

Tutorial - Bonds - solved problems - Tutorial – Fixed income ...

Yield to Maturity

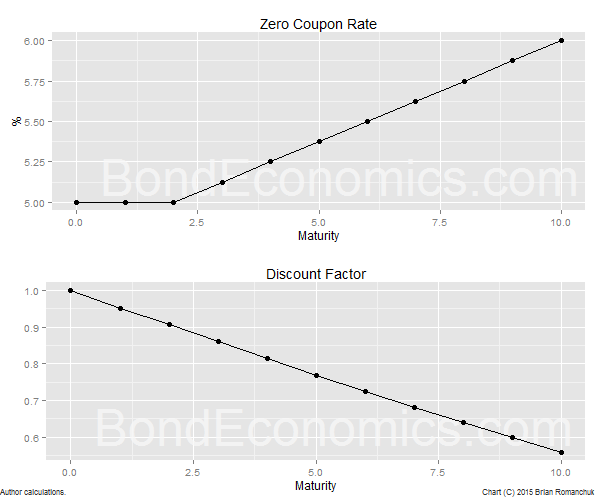

Zero-Coupon Yield Curves - Part I

Bond Economics: Primer: Par And Zero Coupon Yield Curves

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

Valuing Securities Stocks and Bonds. Bond Cash Flows, Prices ...

Zero-Coupon Bond - an overview | ScienceDirect Topics

Fitted Yield on a 6 Year Zero Coupon Bond (THREEFY6) | FRED ...

Solved] Problem 15-7 The following is a list of prices for ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

How Do I Calculate Yield To Maturity Of A Zero Coupon Bond?

Solved] The yield to maturity on 1 year zero coupon bonds is ...

Zero-coupon yield curve for French government bonds estimated ...

Solved The yield to maturity on 1-year zero-coupon bonds is ...

Solved The yield to maturity on one-year zero-coupon bonds ...

10-year zero-coupon U.S. Treasury bond yields and foreign ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

How to Calculate the Yield of a Zero Coupon Bond?

CALCULATING AND USING IMPLIED SPOT (ZERO-COUPON) RATES

Calculating Price and Yield of a Bond Using Zero Curve ...

What is the yield to maturity (YTM) of a zero coupon bond ...

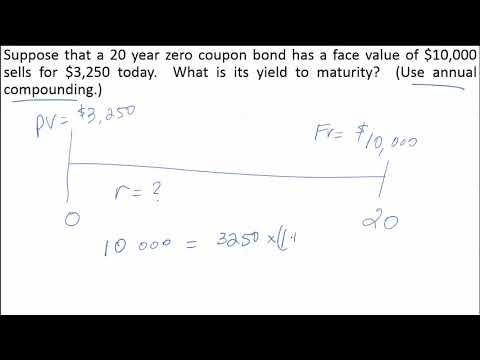

Finding YTM of a Zero Coupon Bond (6.2.1)

Post a Comment for "41 yield of zero coupon bond"